At this point, it should be completely obvious to anyone remotely paying attention that our economy, stock market, bond market and housing markets are 100% dependent on extraordinary bond buying and zero interest rate policy of the Fed. Like a drug addict who has been up for three days popping pills, take away the monetary drugs and the economy will crash hard.

At this point, it should be completely obvious to anyone remotely paying attention that our economy, stock market, bond market and housing markets are 100% dependent on extraordinary bond buying and zero interest rate policy of the Fed. Like a drug addict who has been up for three days popping pills, take away the monetary drugs and the economy will crash hard.

Wall Street knows this, as evidenced by the stock market action this year. In our bizarro financial world, good economic news causes the stock market to fall and bad news causes it to rise, since an improving economy means the Fed may reduce the stimulus a bit sooner. The financial press seems to understand this as their coverage is fixated on every nuance of the Fed’s statements. Yet, while they understand our economy is totally driven by unsustainable Fed policy, they seem content to turn a blind eye to the full implications and enjoy the ride while the getting is good. What’s remarkable is how complacent Wall Street is about the downside risks once the stimulus is removed, whether voluntarily or because the Fed’s hand is forced.

Everyone on Wall Street has the same plan, just ride the markets up while the Fed is printing money, and then when the printing stops, get out at the top before the markets reverse. If you read that sentence and are wondering how everyone can get out at the top, good for you. They can’t. Imagine a large crowd watching an extra-inning baseball game in a stadium with one small exit. Everyone is still sitting in their seat thinking, I’ll just enjoy the game and leave right before the final out to beat the crowd.

In recent weeks since the Fed’s June 19th policy statement, there are signs that the crowd is starting to get a little restless. It’s as if a baserunner reached first and a few of the spectators quietly began to exit while others started shifting their way towards the aisles. Now the crowd seems to be leaning on every pitch from Bernanke. Ball one, the batter may walk and advance the runner closer to scoring the winning run; better inch towards the door. Strike one, he may strike out and the game will continue, better inch back to our seats to enjoy the game.

But the real question is this: On June 19th, did enough of the crowd come to the collective realization, or the Great Realization as I am calling it, that at some point the game must end, and when it does it won’t be pleasant? Did they finally realize that the emperor has no clothes? The market action since then, particularly in the bond market suggests that we may be at a turning point. If this is the turning point, or better yet a tipping point, there is no putting the toothpaste back in that tube. The jig, as they say, will be up.

The Great Realization

Obviously, the Great Realization won’t happen on a single day. To introduce yet another analogy, the entire herd (and Wall Street is a herd) doesn’t turn all at once. First a few cows (or sheep) turn. Then a few more catch on. Then all of a sudden there’s a stampede in the new direction. It will happen in fits and starts. It may have already started. We will only know the exact timing of this process in hindsight.

So how will we know when it has happened? When the Fed announces another increase in QE and the bond market responds by selling bonds. (More on why this will happen below.)

Are we beginning to see signs of movement in that direction? To answer this question we must first examine what Ben Bernanke actually said on June 19th and then look at the market reaction to those statements. The Fed statement said the Fed would continue to buy $40 billion in mortgage backed securities and $45 billion in Treasuries per month and continue to rollover their expiring balance sheet debt. They would also keep the fed funds rate at 0-0.25% for an extended period. In other words nothing changed. Then in the ensuing press conference, Mr. Bernanke hinted that if the economy continues to improve in line with Fed committee expectations, they may begin to moderate (i.e. taper) asset purchases later this year and if that doesn’t slow the recovery, they may continue to taper the purchases in the first half of 2014 and ultimately end them in mid 2014. He also quickly pointed out that if conditions worsened, they may increase the amount of monthly bond purchases.

If you actually read the statement and press conference, it was pretty innocuous, even dovish. Mr. Bernanke went out of his way to assure market participants that the Fed wouldn’t remove stimulus pre-maturely and would closely monitor any affects of stimulus reduction. But that reassurance wasn’t enough for a market addicted to ever increasing amounts of monetary crack cocaine. The mere idea that their drug pusher may start to give them less drugs at some point in the future, at a time when they are craving bigger doses to get high, was enough to send them into a tizzy. Stocks, bonds, commodities (particularly precious metals) all sold off on the news. I think Bernanke was completely surprised by the negative market reaction to his carefully crafted statements. Since then, the Fed has been in damage control mode, sending its minions out to the press to “clarify” the remarks.

You see, the Fed, and Ben Bernanke in particular, is in a peculiar situation. Their job is not to tell the truth or even to do what’s best for the economy in the long run. Their job is to maintain confidence- confidence in the economy, in the dollar, in bond prices. They know that without confidence, our over-indebted, over-promised, over-leveraged economy falls apart. They must walk a fine line with their policy statements. They must assure the markets that they can exit the extraordinary monetary policy any time they want, and at the same time they must assure the markets that they never will. They must maintaing the illusion of control which is why they have come up with the analogy of driving a car, where the Fed can press or release the gas pedal to keep the economy moving at just the right speed.

The fact that markets reacted so negatively to the June 19th statement shows that the Fed may be losing their power to walk that tightrope and maintain confidence. It’s like that moment in the Wizard of Oz when Toto pulls back the curtain to reveal that Ben Bernanke is not some all powerful wizard who can steer the economy like a car, but a little man pulling levers behind a curtain, maintaining the illusion of power with parlor tricks. It’s as if the market had some kind of… realization.

As sharp as the market reaction to Bernanke’s statements may have been, the sell-off is not that big of a deal in and of itself. After all, if the threat of a taper was the only reason markets sold off, Bernanke could hold a press conference tomorrow and say that new economic data suggests that the Fed won’t begin to taper and will instead increase bond purchases.

[Edit: Actually, Bernanke did just hold a press conference. He is terrified of the taper. He saw the disruptions in the bond market that occurred at the mere mention of the possibility of a taper and can only imagine the disastrous affect on an already fragile economy if he actually began to reduce the size of Fed asset purchases. (Never mind actually unwinding the balance sheet.) Just watch the quivering address he gave today as he tried to reassure markets that the Fed won’t be tightening any time soon.]

But what if the market reaction is driven by more than just taper talk? What if it’s a broader realization that the Fed has NO exit plan? What if the bond vigilantes have finally awaken from their comma and the low for bond yields is in?

How will the economy, stocks, bonds, housing, and precious metals fare when the Fed loses control of interest rates? I address some of the highlights below.

The Economy

The taper speculation is based on what is perceived to be an improving economy. The Pollyannas on Wall Street mistake rising asset prices such as stocks and real estate for an improving economy. They look at headline jobs numbers and note that the unemployment rate is slowly but surely coming down.

The truth is, the real economy is in dire straights. The number of Americans on food stamps is at record highs and growing at over 47 million. Americans receiving disability benefits has risen for nearly 200 straight months to 11 million. The May trade deficit was $45 billion. The headline unemployment is stuck at 7.6% even as more people leave the labor market and the broader U6 unemployment spiked up .5% to 14.3% in June. The heralded jobs number for June of 165,000 new jobs was actually a loss of 157,000 full time jobs that were replaced with 322k part time jobs. (Due in no small part to Obamacare.) Q1 GDP was revised down to 1.8% annualized (and that’s if you believe the government that inflation is only 1.4%).

So, with the economy teetering on the brink and short term interest rates already at zero, what would happen if Bernanke were to reduce his bond purchases? Basically, the crisis of 2008 would return with a vengeance. Mortgage rates would rise sharply which would send housing prices lower. The interest based assets on bank balance sheets would decline in value requiring banks to sell assets to raise capital. Since banks are so highly levered in an attempt to conjure up yield, a drop in asset prices will cause many banks to fail as was the concern in the 2008 financial crisis. Bond funds, many of them highly leveraged to chase yield, held largely in retirement accounts will tank in price. The cost of borrowing for the government will increase meaning more of the budget will go towards simply paying interest on the debt. And these are just the tip of the iceberg.

The Bond Market Time-bomb

Write this down: The bond market is the key to everything. What Mr. Bernanke is really terrified of is rising interest rates. Interest rates have been falling for 30 years and the last decade or more of that has been artificially driven by the Fed creating the mother of all bubbles in the bond market.

Recently, interest rates have begun to tick up, boosted by the taper talk. If interest rates continue to rise despite all of the Fed’s intervention it’s game over. And rise they must; it’s only a matter of time. The interest rate suppression is like holding a beach ball under water. When Bernanke, finally loses control, expect rates to shoot up past the market equilibrium. And when that happens, shit will be hitting every fan in sight. Better yet, it will be like a shit storm passing through a windmill farm.

The Fed controls short term rates by setting the overnight rate it lends to banks, currently at 0%-0.25%. This is their traditional means of stimulating the economy as lower rates encourage banks to loan more money, thus generating economic activity. With short term rates at their zero bound, the Fed has added the “unconventional” (i.e. balistically insane) tool of purchasing longer term Treasury bonds and mortgage securities. This reduces the supply of bonds in the market and increases the demand which raises bond prices which lowers rates. This year the Fed has purchased (i.e. monetized; i.e. printed money) 90% of all of the debt issued by the federal government.

But the real effect of the Fed’s bond purchases is that it has the added benefit of encouraging others to buy bonds since they feel the Fed will keep bond prices from falling. I’ve said it before but this point cannot be overemphasized: No one is buying 10 year or 30 year bonds to clip coupons at record low rates until maturity. They are buying them with the intention of collecting some yield and then selling them to a greater fool. (because the Fed has announced they will be the greater fool.)

While it’s easy to see how the Fed’s bond buying pushes rates down, it’s less obvious to see how Fed bond buying will cause rates to go up when the Great Realization hits. Here’s the gist of it.

1. The bond market is huge with Treasuries held by the public over $11 trillion and the total U.S. bond market over $40tn.

2. The Fed buying bonds is the equivalent of printing money which debases the currency. This is in-and-of-itself inflation and eventually shows up in rising consumer prices. (To date, much of the inflation hasn’t shown up in rising consumer prices as it has been fighting deflationary credit contraction and bidding up stocks and homes. Although, oil prices above $105 suggest that is changing.) More bond buying means faster debasement which means rising expectations for future inflation.

3. As bond holders realize they are being paid back in debased currency, they sell bonds and require higher yields to buy new bonds. There is a threshold where the Fed’s purchases cannot keep pace with sales from the market spurred on by… Fed purchases.

That is the tipping point. That is the Great Realization. It may already be happening as foreign central banks sold a record $32.4bn of Treasuries in one week. Similarly, investors pulled $80bn out of bond funds in June.

For individual investors there is absolutely NO reason to own bonds. And if you have a 401k or an IRA you probably do own bonds. The yield on 5 year Treasuries is barely keeping up with the governments bogus inflation number. And the downside risk of falling bond prices is significant. (We tend to forget bonds can lose money after 30 years of rising bonds.) And by all means run from leveraged bond funds like the plague. Many investors are finding this out the hard way as some leveraged bond funds have dropped 20% even 30% in one month following a whiff of taper.

If you need income from your investments, I would suggest looking into relatively safe, dividend paying stocks in areas of the world with more stable economies. In addition to receiving higher yields without leverage, you have protection from inflation by owning shares of a company.

The Stock Market

The stock market has had a great run so far this year up 14% and more than doubling since there lows from 2009. In my opinion, with all of the black swans flying around, now may be a good time to take some profits.

QE and historically low rates has been very kind to stock prices which, like everything else, are priced by supply and demand. The freshly printed money has boosted demand and low rates allowed many companies to borrow money or use excess cash to buy back shares, reducing the supply of shares and increasing earnings per share. Also, the crash of 2009 forced many companies to streamline their workforce which has boosted the bottom line.

The big picture for stocks, however, is not great. While QE inflation will continue to provide a tailwind for equities, I think the gains of equities will be hard pressed to keep up with the rise in the cost of living. And the hiccup in stocks after the June 19th press conference reminded markets that stocks can fall if the Fed’s easing is dialed back.

Top line sales are stagnant and the workforce has been squeezed for every last drop of juice. Ask yourself who are the customers of U.S. companies? Are they a generation of grads loaded up with student loan debt and poor job prospects? Are they retirees who’s bonds are paying them close to nothing for additional income? Are they homeowners who could see there home equity dry up again?

I’m not saying get completely out of stocks. There is a lot more money printing to be done and it’s better to own real things like companies than pieces of paper the come off of Bernanke’s printing press. I think owning solid companies that sell to growing markets is a critical part of any investment portfolio. I’m just suggesting that now might be a good time to reduce one’s percentage allocation to domestic stocks and look for alternatives (Hint: see the gold section below.)

Charles Biderman of Trim Tabs just posted an excellent simplified explanation of why stocks could fall 30% even without any major catastrophes. In short, P/E multiples are around 15 times earnings which is fine in times of good growth. However, with today’s sluggish growth, P/Es of 10 are more consistent with historical periods of similar growth.

Real Estate

One of the big propaganda pieces foisted on Americans is the notion that owning a home is an investment. Income producing rental property is an investment, but a private home is simply a place to live (that needs constant upkeep). The equity in your home is an asset while the mortgage is a liability, the values of which can rise and fall with market conditions.

The run-up in housing prices since the crash has been supported by record low interest rates and more recently by speculative buyers such as Blackstone buying up houses with cash (leveraged to the hilt of course) as an “own to rent” investment. The false low interest rate signal also cause new housing starts to increase. Since the supposed recovery is predicated on a housing recovery, it’s worth exploring further

There are growing concerns that the peak of this re-inflated bubble might be in. (All real-estate is local so I’m dealing in broad terms here.) With interest rates rising, the refi-market (which was a big chunk of the mortgage market) will completely dry up once the last few stragglers scramble to lock in low rates before they rise even more. As rates rise, prices must fall to keep mortgage payments affordable. Also, payments on adjustable rate mortgages will rise in a replay of 2008.

And who do we expect to buy (or rent) all of these new houses? Baby boomers are retiring and if anything will be downsizing. College grads, historically the source of new home formation already have a mortgage called a student loan and seem more than content to live at home with Mom and Dad.

My bet is that Blackstone and others will take a bath on their own to rent housing play as mortgage rates rise. As they try to exit the market, all of that spec buying will turn into a flurry of spec selling. For a great anecdotal example that we are in a new housing bubble, check out this incredible story about the Las Vegas housing market.

Gold and Silver and Oil

In December of last year I posted a two part article basically saying that gold and silver prices could take off any day and now (12/20/12) would be a good time to add to your positions. In hindsight, the timing of that article was, for lack of a more honest word, unfortunate. Since then, the S&P is up 16% while gold and silver are down 22% and 32% respectively. Ouch.

Of course, I have never claimed to be a market timer. Nor did I say sell all of your stocks and put everything into gold. Instead I have advocated accumulating gold and silver on the dips as you build up your position for the endgame in which I see gold and silver going up 5x, 10x or more in dollar terms. And at the time, it seemed like a good entry point based on the fundamentals and market conditions. And if you read those articles part 1 and part 2 you will see that everything I said still applies despite the price drop.

So am I licking my wounds after the beating the metals are taking? On the contrary, the recent price smash sets us up for a bigger, faster, more meteoric rise in the near future. My only regret is that I don’t have the dry powder to buy more at these prices. Allow me to explain…

First, let me say that if you bought ten silver coins in December (assuming you didn’t sell them) you haven’t lost anything. You still have ten silver coins. The dollar price quote on this particular day is irrelevant if you do not intend to sell. As Rick Rule likes to say, in the short term, the market is a voting machine; in the long term it is a weighing machine. What we have seen in recent weeks is the traders voting that the price of gold and silver should go down.

As I have mentioned before, the “price of gold” is not determined by physical gold trading hands. It is set by the futures markets trading paper gold contracts with huge amounts of leverage. The recent price action of gold and silver proves this, as the price the price has been falling at a time when demand for physical metal is going through the roof. The selloff in gold was entirely leveraged speculators who don’t own any physical gold selling paper contracts to other speculators who don’t really want to own any physical gold.

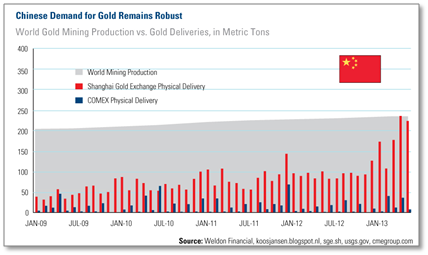

The cause of the gold price takedown is a complicated long story and I won’t get into it here, but the effect of the price drop has been unmistakeable. Huge amounts of physical gold and silver are being scooped up by people in China, India, Japan as well as emerging market central banks. They are taking advantage of the low prices to acquire as much physical metal as they can get their hands on. What we are witnessing is nothing less than a shifting of the world’s wealth from West to East. As the chart below shows, the physical off-take from just the Shanghai Gold Exchange in the past few months has equalled the entire world mine production.

The other, related effect is that gold is shifting from weak hands to strong hands. It’s shifting from speculators who view gold as a trade (weak hands), to owners who want to hold onto gold to pass their wealth on to future generations (good luck prying it out of their hands). And it’s shifting from Western central banks, who view gold as a threat to their currency hegemony, to Eastern central banks who view gold as a way to legitimize their currencies.

At $1200 gold and $20 silver, the price of the metals in under the average all-in cost of mining the metals. That means gold companies would be better off just buying gold on the market than going out and digging it out of the ground. These prices can’t last long or miners will take huge chunks of production and exploration off line.

With bearish sentiment for the metals at all time highs, now is a great time to back up the truck and buy, buy, buy. Maybe sell some of those bubblicious bonds that are in your retirement fund or take some profits on your high flying stocks to buy gold and silver at bargain basement prices. Can the price of gold and silver drop more? Sure. But the goal is not to pick the absolute bottom. The goal is to accumulate as much as you can before you can’t buy physical gold or silver for any price.

I could probably write ten more pages on the bullish case for gold and especially silver. (But I’m tired) The information is out there. It’s up to you to do some research on recent events in the gold market. http://goldsilver.com/industry-news/ is a good place to start. Perhaps scroll back to June 19th and begin reading.

One quick note about gold stocks. The low price of gold and silver has been rough on gold mining companies. Mining is a very difficult business with huge input costs, multiple variables and unknowns, and political risks. Many of the experts I follow believe that as many as 80% of the mining companies, particularly juniors and exploration companies may be out of business in a few years. However, the companies that do well can see explosive upsides to their shares. If you have a high risk tolerance and want to speculate in the mining shares I would recommend finding a broker who specializes in that sector with a great long-term track record.

One quick note about oil. It’s interesting to point out that oil is blasting higher as gold and silver fall. While the oil price is susceptible to being pushed around by speculators, the price is more tied to the physical commodity because it gets used up constantly. The high oil price suggests we are finally seeing cost push inflation (despite the government wanting to blame it on turmoil in Egypt) which is bullish for gold and silver.

![[Most Recent Quotes from www.kitco.com]](https://i0.wp.com/www.kitconet.com/charts/metals/gold/t24_au_xx_usoz_4.gif)

![[Most Recent Quotes from www.kitco.com]](https://i0.wp.com/www.kitconet.com/charts/metals/silver/t24_ag_xx_usoz_4.gif)

Great insight! Glad that you pointed out the problem of underemployment and how the reporting of unemployment does not take into account underemployment. Looking forward to the next post!

You have to wonder how much time we have before it implodes!!!

Idk if its best to invest in silver bullion at this time, seeing as it really hasn’t exploded like some experts said it would.

Hello, i think that i saw you visited my weblog so i came to “return the favor”.I’m trying to find things to improve my web site!I suppose its ok to use a few of your ideas!!